EschCollection

Dear readers/followers,

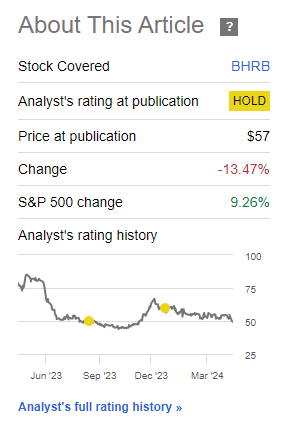

My last coverage of the financial company Burke & Herbert and the associated merger with this stock was done at a conviction or rating of “HOLD”. This turned out to be the right choice for investors, as the company has moved down double digits during a time when the S&P500 is up almost 10%. You can see the result below, and you can find my last article, with the aforementioned neutral rating here.

Seeking Alpha Article RoR (Seeking Alpha Article RoR)

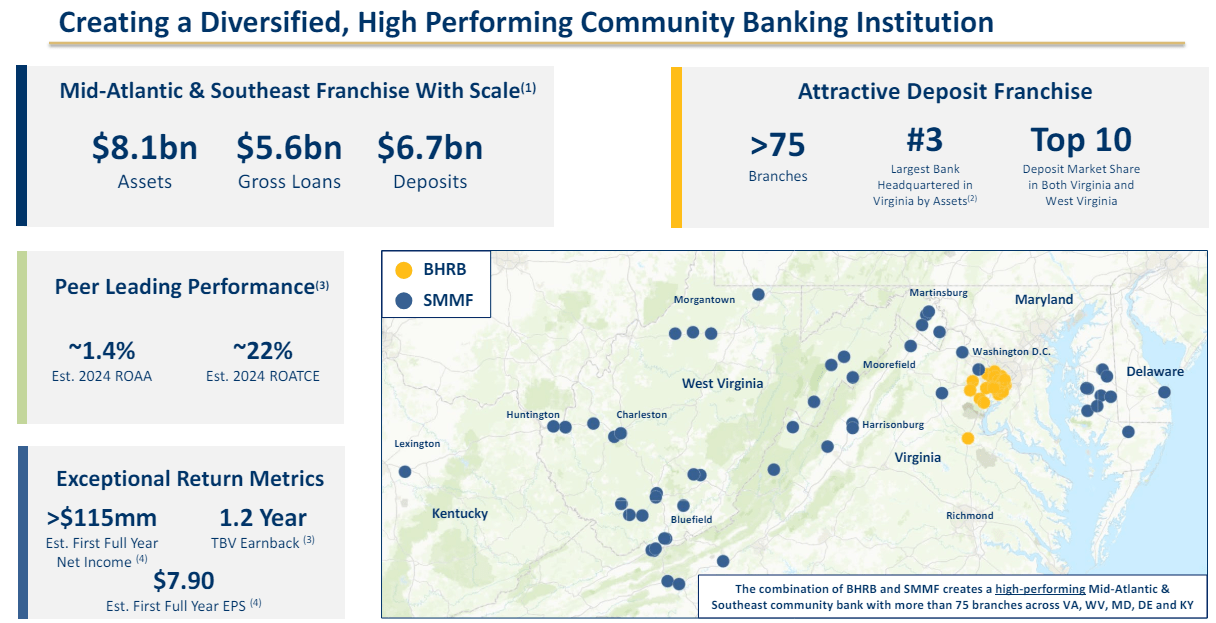

In this article, I’ll update on Burke & Herbert as a company. When I last wrote about it, the merger had been finalized which overall will enhance its position and overall appeal – at least how I saw it, resulting in a bank with over $8B in assets and is expected to have a 2024E ROATCE of 22% and ROAA of 1.4%.

Again, all of this can be characterized as an attractive set of fundamentals – but that does not mean that Burke & Herbert is necessarily a business that we want to invest in, at least not at this price.

For now, the market seems to share this view and agree with that assessment here – for the company is down quite a bit.

Let’s look at the recent results and see if there is an upside to be had here.

Burke & Herbert Company update and 1Q24 review – The company has some positives, but uncertainties remain

Fundamentals has never been a problem for this business. 150 years of operational relative stability with a focus on the American capital of D.C and its areas is an easy thing to like. The added appeal with the merger with Summit has resulted in natural scale advantages, and the bank has some potential to deliver not only a better customer experience thanks to this new structure, but also significant cost savings as it can cut operational costs. It might, as of yet, be too early to see the effects of these cost savings or even the scale that’s possible, but there’s likely to be some appeal here.

What I like fundamentally about Burke & Herbert is that it reminds me in some ways of the still-successful Swedish banks with stronger ties to the communities and neighborhoods that they operate in. I don’t mind investing in multinational banks – but some success that I’ve found has been identifying strong, low-leveraged regional players with strong ties to the customers and buying them cheaply.

For the 1Q24 period, Burke & Herbert have started reporting the operational results from the two banks together, and we can annualize these to get an idea of where things are likely to go. That’s also why 1Q24 resulted in some downtrend for Burke & Herbert – because the results were not fantastic.

With an overall net income of just above $5.2M, the company annualized at around $20.5M, which is lower than the FY23 numbers. NII is up, but the rest of the results are somewhat mixed.

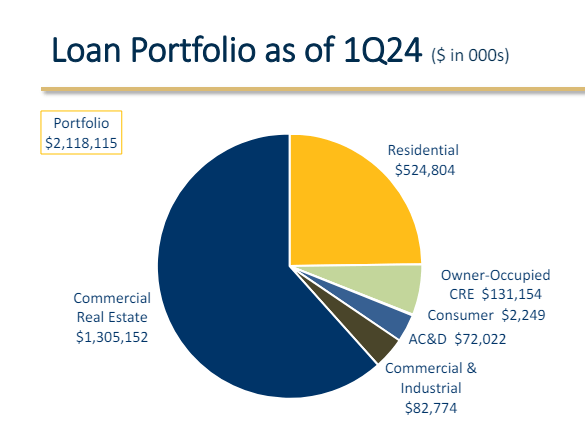

There’s also the fact that the company’s loan portfolio has a non-trivial exposure to CRE.

Burke & Herbert IR (Burke & Herbert IR)

You may even argue that we can lump the so-called owner-occupied CRE and other segments under the general CRE, which would put this close to 70% of the total loan portfolio, now totaling as you can see just over $2.1B.

What sort of assets does the company have exposure to then? How bad is this CRE?

Well, over 1/4th of the company’s loan exposure is in retail real estate. That can be a bit of a red flag, but it also pays to remember that we’re talking a very attractive geography here. The loan geographic footprint is spread across greater DC, Maryland, and the Virginia DMV area, with minimal office building exposure within the D.C proper. Instead, the company’s focus is on commercial and industrial loan growth.

Do we like this?

Sort of – the company, having survived multiple downturns and crashes, clearly knows something of what it does, and I don’t see any immediate risks for the company’s loans, beyond what macro dictates here. If asked how I view the potential future based on the bank’s loan structures, I would answer I view this generally neutral – the risk of the CRE made up by the excellent geographies.

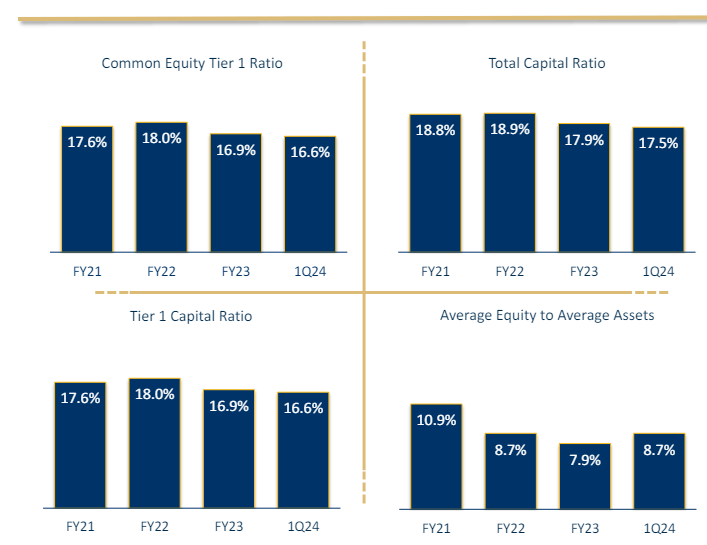

However, that does not make this a good play. The company’s capital trends are declining/growing more negative.

Burke & Herbert IR (Burke & Herbert IR)

The company has also seen a quite significant spike in NPLs, from an FY23 number of 0.18% to a 1Q24 number of 1.24%. Not at any level that I would consider even close to fundamentally dangerous, but I do like banks and financial institutions that keep it firmly below 0.5%.

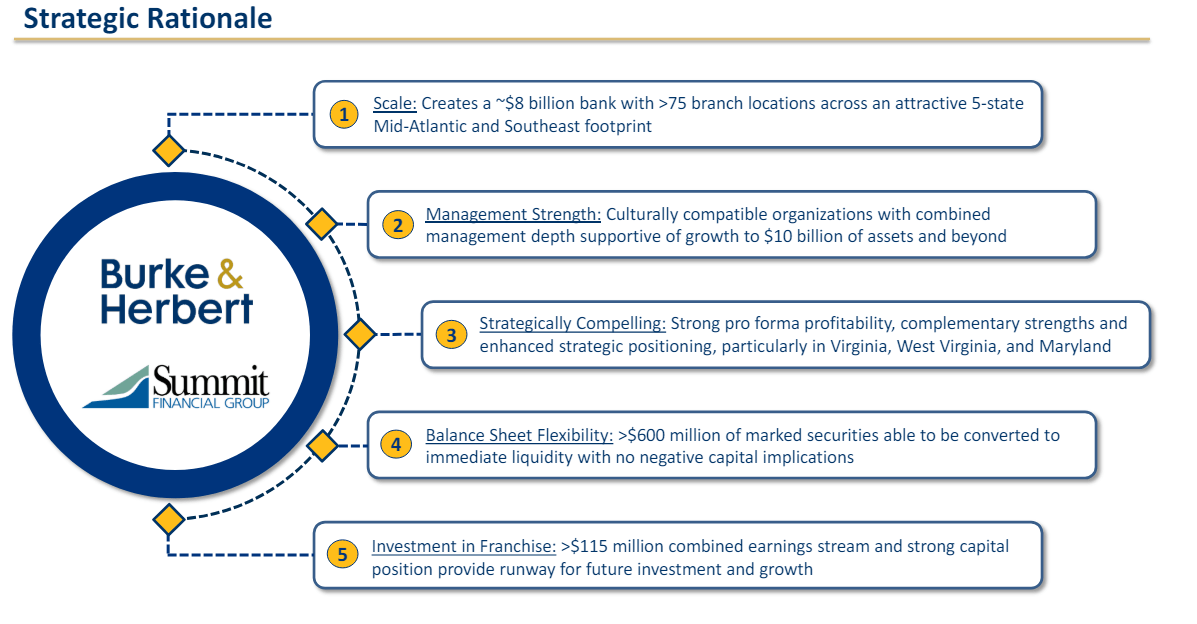

Once the merger with Summit is finalized the company’s assets will grow to over $8B, and 75 branches – turning Burke & Herbert from a DC-based player into a more regional bank with 75 branches across multiple states, including Virginia, West Virginia, Maryland, Delaware and Kentucky – with more than 800 employees that work for the bank.

Burke Herbert IR (Burke Herbert IR)

This is obviously a non-trivial expansion of the company’s overall operations, as well as the bank’s overall risk profile. We still don’t have the results for this merger, so what we’re seeing in 1Q is the legacy of Burke & Herbert only – for further upside, we need to wait. However, given the valuation movements, it seems clear to me that the market is not thrilled about the prospect here, and has taken a passive position.

What I want to make perfectly clear to investors is that I see relatively few operational and fundamental reasons for a deep investment into Burke & Herbert, unless this is done at a significantly positive valuation. Why? Because if we look at the margins and return metrics for Burke & Herbert when compared to other banks is quite average – the company’s yield is less than 4.5%, and we’re talking about this in an environment where it’s possible for you to get around 5% from an A-quality bank like Toronto-Dominion (TD), or even more from something like The Bank of Nova Scotia (BNS), or 3-4% from any savings account.

Let’s look at what the valuation tells us, and whether there is any idea in investing in a bank with a total market cap of $370M as of today.

Burke & Herbert – a sub-$500M market cap bank and the valuation & potential upside

The unfortunate fact of the matter is that Burke & Herbert remains a very speculative play. In order for me to invest comfortably in this business I would have to pick up the assets for a significant discount to the book – but at such a discount, the question would simultaneously be raised if this is even a good idea given what such a discount would imply.

The valuation for this company remains very tricky to estimate. Given its very small size compared to banks on a larger scale, the lack of clarity on the upside following the merger, and the overall macro, where this company is certainly more impacted than a larger bank by higher funding costs, I would generally want to pay less than I would for a larger bank. I would be very curious to hear disagreements as to that assertion, given the scale efficiency that larger banks have.

Yes, the company’s focus on its customers is encouraging – but it’s exactly this that I question if the bank will be able to maintain, given that the merger expands the bank’s operations to a whole host of other states. Will Burke & Herbert remain the community-oriented, small bank that has made it successful, or will it become one in a line of riskier, small regional banks that we all know and some of us follow?

The proposed mix of assets certainly suggests an increase in risk and a dilution of Burke’s geographical advantage in exchange for scale-related cost decrease and a larger customer base.

Burke & Herbert IR (Burke & Herbert IR)

I do not live in America, but due to investing there, I learned a lot about the country – and even I know what sort of risk profiles and geographical advantages and disadvantages you can see in areas in “coal country”, such as Virginia centered around Bluefield. That does not make these areas uninvestable by any stretch of the imagination, but my point is that the risk profile is very different.

Like with previous articles, I do not view this investment as a favorable one. I’d still say that for a cheaper price, I can buy the 5.15%-yielding Toronto Dominion Bank, which comes with an AA-rating in credit and a market cap of $133B CAD, and that comes with a substantial, conservative upside even if the bank goes essentially nowhere from here.

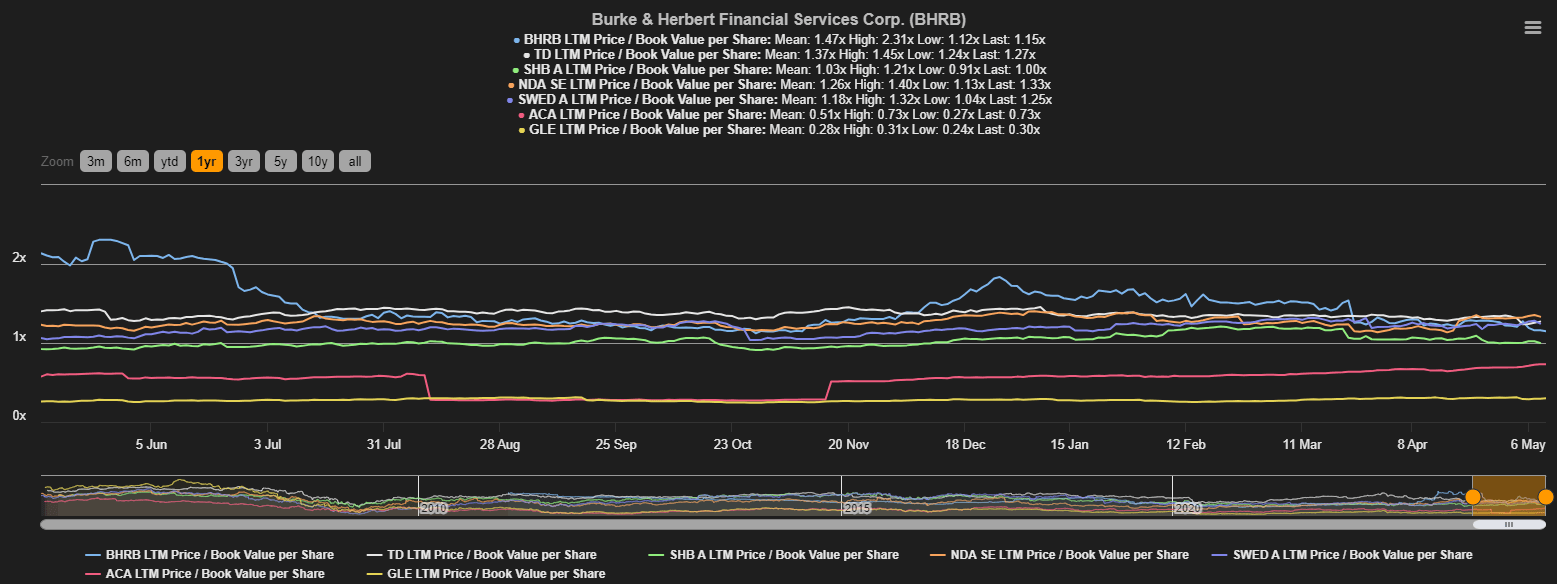

I make a very simple comparison here that even at a share price of around $50/share, this company’s book value, or assets, are traded at a multiple of 1.15x. Take a look at where some of the banks I invest in are trading with regards to this multiple.

Tikr.com Burke & Herbert Asset valuation (Tikr.com Burke & Herbert Asset valuation)

This metric is not the end-all-be-all of anything, but it gives us an indication, and this indication runs through all of the relevant metrics. Burke & Herbert is not significantly undervalued even next to world-leading or nation-leading banks that I invest in – and if I am supposed to take that sort of risk that Burke & Herbert represents, I would not do so at this valuation.

Because of that, my updated thesis for Burke & Herbert is as follows.

Thesis

- Burke & Herbert is an interesting regional banking play in a mostly attractive area of the United States. While this company lacks the appeal of any larger or global bank that I usually invest in, it does have meaningful potential upside to a normalized post-transaction P/E level of 10-12x based on a $7-$8 EPS.

- However, even if such a valuation is possible, I would view it as a risky business to expect this out of a bank like this in an environment like this. This is one of those investments that I wish could be attractive, but the fact is that on a comparative basis, it is not.

- Put into context, I can buy BHRB – or I can buy a 5%+ yielding Toronto Dominion, with an A+ credit rating, and a significantly better conservatively-adjusted upside available than this one.

- In such a situation, my choice is obvious. This investment is contextually speaking, a “HOLD”, even though upside is possible.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I can’t give a higher rating or upside to a company in the midst of a merger and the associated uncertainty this brings, and now added to by the overall macro and uncertainty, which in my perspective, really hasn’t improved since I last covered the company.

This remains a “speculative investment”, despite my current PT. I will revisit this where possible, but to those requesting coverage, I would look at non-regional and more “global” banks at this particular juncture.

{kind=link}