Nikada

As we entered 2024, I wrote an article – The Battle Of Two Goliaths: Ares Capital Vs, FS KKR, Which One Will Win In 2024? – comparing two largest BDCs with an aim to determine, which one of them will deliver superior returns in 2024.

While the analysis suggested that both Ares Capital (NASDAQ:ARCC) and FS KKR Capital (NYSE:FSK) are inherently attractive investment choices, the conclusion was that FSK is better positioned to register solid return this year, outperforming ARCC.

The reason for that really lies in the massive discount to NAV, improving investment portfolio dynamics of FSK, and much higher yield than what is offered by ARCC.

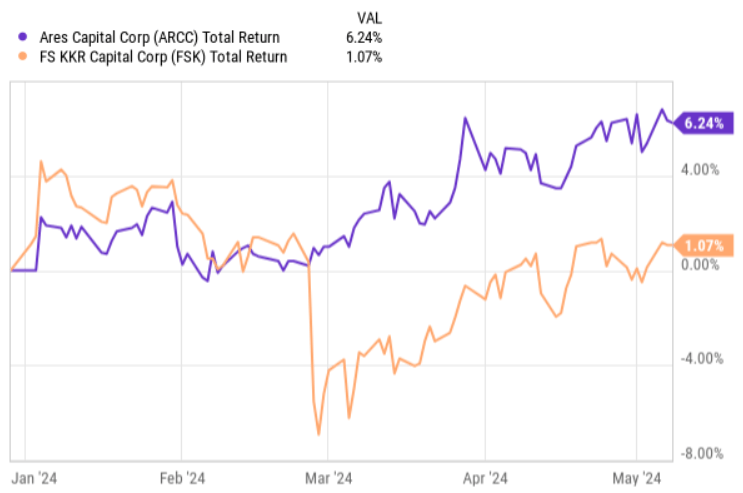

However, since then, ARCC has clearly delivered better total returns than FSK on a YTD basis.

Ycharts

While at the early start of this year, FSK did indeed assume a strong recovery process (i.e., price convergence to the underlying NAV), as soon as the Q4, 2023 earnings deck was circulated, all of the previously registered gains were effectively destroyed. The key catalyst here was FSK’s struggles on the non-accrual end, which in combination with declining funding volumes imposed a notable pressure on the adjusted NII generation. This, in turn, raises serious questions by the market around the overall sustainability of FSK’s dividend.

Nevertheless, peeling back the onion a bit (i.e., making an analysis about Q4, 2023 data points), I still saw a reasonable potential for FSK to actually outperform ARCC and / or the overall BDC market in 2024.

Now, just recently FSK issued its Q1, 2024 earnings report, which reveals a set of new and interesting data points, which are worth contextualizing with the bull thesis.

Let’s now review the recent earnings deck and decide whether FSK is still a buy.

Thesis review

All in all, the key metrics measuring FSK’s operating and portfolio level performance came in strong with some signs of improving dynamics. If we look at one of the most important measures – NII per share – we will notice quite a notable jump relative to the prior quarter. NII per share for Q1, 2024 landed at $0.76 per share, as compared to $0.71 per share, for the quarter ended December 31, 2023. Here it is hard to distinguish a specific driver that contributed to the uptick in NII per share, but instead it was a combination of some top-line and expense items, which slightly improved over the quarter. For example, other operating expenses and interest expense came in lower than in the prior quarter, and the income from the fee side went up ~ $5 million.

However, on an adjusted NII per share basis, FSK recorded a slight drop from the previous quarter (i.e., $0.75 per share this quarter compared to $0.73 per share in Q4, 2024). The reason for this is simple – in the previous quarter FSK benefited from a positive adjustment of an excise tax of about $18 million, which made it per definition a tougher comparison than normal.

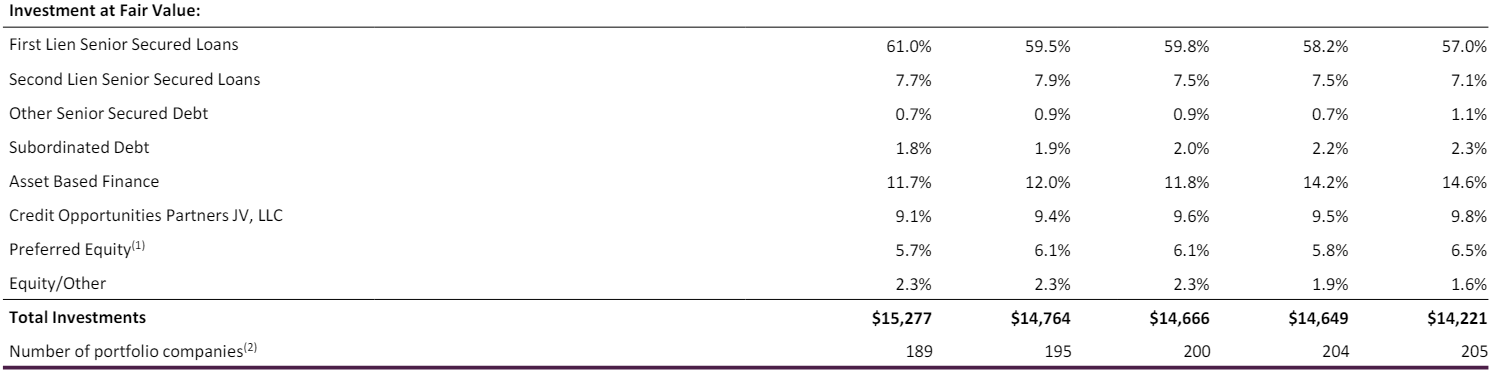

FSK Q1 2024 Earnings Supplement

Now, turning to portfolio level metrics, the table below indicates a positive momentum (or rather a continuation of it), where we can see how FSK has been taking dedicated steps in enhancing the quality of its portfolio.

On the surface it might seem that the quality is deteriorating as the exposure to first lien loans steadily declines. However, the part of portfolio that comes from the reduction in first lien position has been mostly shifted towards an even more defensive segment like asset based finance.

FSK Q1 2024 Earnings Supplement

Granted, there have been some increases in other investment segments that are not so defensive (e.g., preferred shares and subordinated debt), but these are really minor movements in the context of total exposure.

Importantly, the yield metrics have not suffered. The weighted average annual yield on all debt investments was 11.4% compared to 11.2% in the prior quarter. Excluding the impact of merger accounting, the weighted average annual yield was still circa 20 basis points higher than in Q4, 2023.

It is also worth underscoring the major improvements at the non-accrual end, which has been one of the drivers of the prevailing discount to NAV. During this quarter, the Management did a great job in bringing down the non-accruals from 5.5% in the last quarter to 4.2% now (if measured on a fair value basis). Most importantly, there were no meaningful additions to the non-accrual position (already for a second quarter in a row) sending a strong message about the stabilization of portfolio quality.

The only negative aspect that we have to factor into the equation is the negative investment activity, where the sales and redemptions clearly exceeded the new investment made. The problem with a declining portfolio base is that it makes maintaining or growing the NII generation more difficult as there is just smaller pool of assets from which to capture spreads between portfolio yields and cost of funding.

FSK Q1 2024 Earnings Supplement

With that being said, I would not make any meaningful conclusion from this data point, especially knowing that the last two quarters resulted in net positive investment flows and the total investment activity for this quarter reached the highest amount (volumes) in the TTM period.

The bottom line

In a nutshell, Q1, 2024 earnings results were solid. The NII per share meaningfully improved rendering the dividend coverage ratio healthier and more sustainable. The improvement was registered despite the negative net investment activity and a notable reduction in external leverage.

My most important takeaway from this quarter was that it seems that non-accruals have finally stabilized, which should enable FSK to gradually revert back to the adjusted NII levels that are closer to $0.80 per share level (as the headwinds from write-offs dissipate).

Given the aforementioned dynamics and still existing price to NAV discount of ~ 22%, FS KKR Capital remains a clear buy for me.

{kind=link}