liorpt/iStock Editorial via Getty Images

Thesis

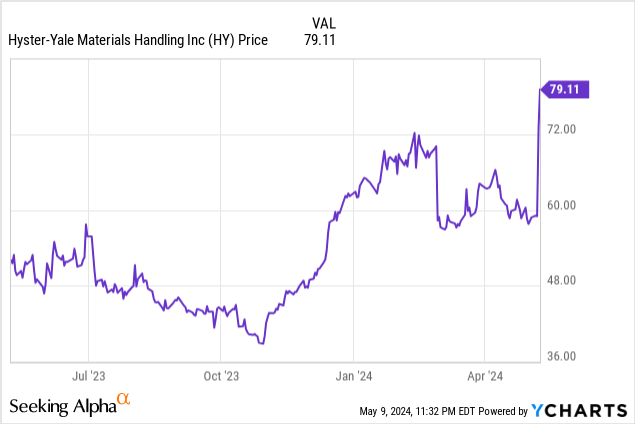

On Tuesday, May 7, 2024, Hyster-Yale Materials Handling, Inc. (NYSE:HY) posted its first quarter-2024 earnings report. When markets opened the next morning the stock price shot up, closing 23.55% higher. The following day saw the price jump again, by another 8.35%. Altogether, the stock price climbed from $59.02 to $79.01 in the space of two days.

Was there something incredibly huge in the earnings announcement from the lift truck company? No, but it was a solid report with revenue of $1.1 billion, $70 million more than predicted, while its GAAP EPS of $2.93 beat estimates by $0.79.

What it told investors, especially those who sold in the wake of the fourth-quarter 2023 earnings report, was that it was back to business as usual. The jump in the stock price was a rebound, getting it back on the trajectory it had been on before the Q4-2023 earnings took it down.

Hyster-Yale is back in the growth game, and I have rated it a Buy.

About Hyster-Yale

The company’s history begins in the 1840s, when Linus Yale Sr. began designing and manufacturing a series of high-security locks. In 1920, the company purchased a firm that had developed the first battery-powered low-lift platform truck (information from the company website).

The Willamette-Ersted Company is formed in 1929, to manufacture winches and lifting machines. As Hyster-Yale explained on its website, “Legend has it that loggers using the equipment would cry out “hoist er” as they prepared to lift a load. The expression, spelled out as Hyster stuck, marking the beginning of the storied Hyster lift truck history.” Lift trucks are also called forklifts; the terms are interchangeable.

In 1989, the two companies come together under NAACO Industries, Inc. and subsequently become the NAACO Materials Handling Group. Following the Group’s spinoff by NAACO Industries in 2012, the company became Hyster-Yale Materials Handling, Inc.

There’s one more name change in the works; on May 31, the corporate title will become Hyster-Yale, Inc. At the same time, its wholly owned subsidiary Hyster-Yale Group, Inc., will become Hyster-Yale Materials Handling, Inc.

The company described itself in its 10-K for 2023 as, “a globally integrated company offering a full line of high-quality, application-tailored lift trucks and solutions aimed at meeting the specific materials handling needs of its customers.”

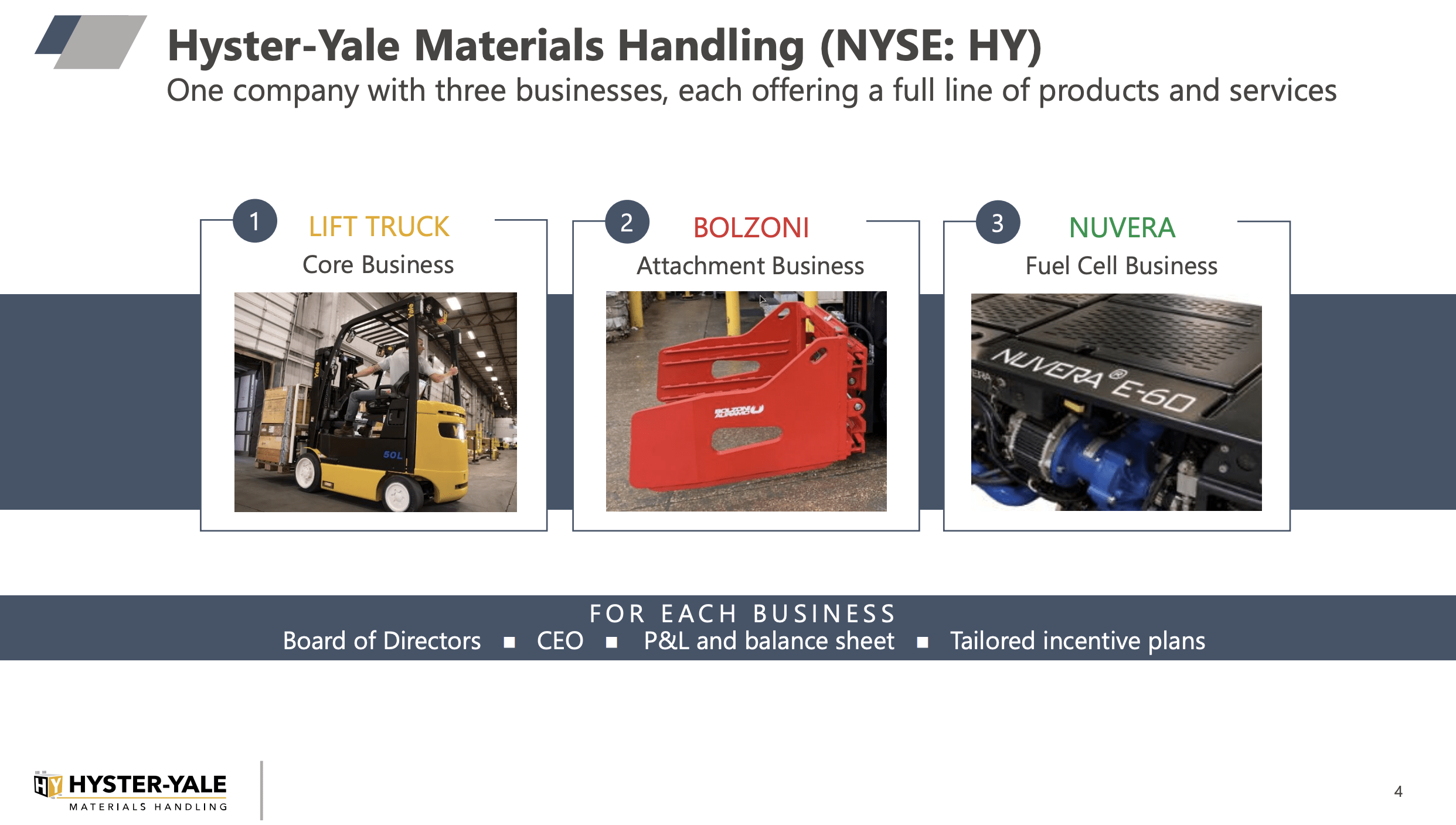

Those solutions include a comprehensive line of lift trucks, aftermarket parts, and attachments for those trucks (Bolzoni), as well as a fuel cell company (Nuvera):

HY Segment slide (Q1 company presentation)

The company broke out 2023 revenue by components in the 10-K:

- Lift trucks: 74%

- Parts: 15%

- Service, rental, and other: 6%

- Bolzoni: 5%

- Nuvera: less than 1%.

Geographically, Hyster-Yale derives most of its revenue from the Americas:

- Americas (North America, Latin America, Brazil): $769.7 million.

- EMEA (Europe, Middle East, Africa): $199.4 million.

- JAPIC (Japan, Asia Pacific, China): $37.7 million.

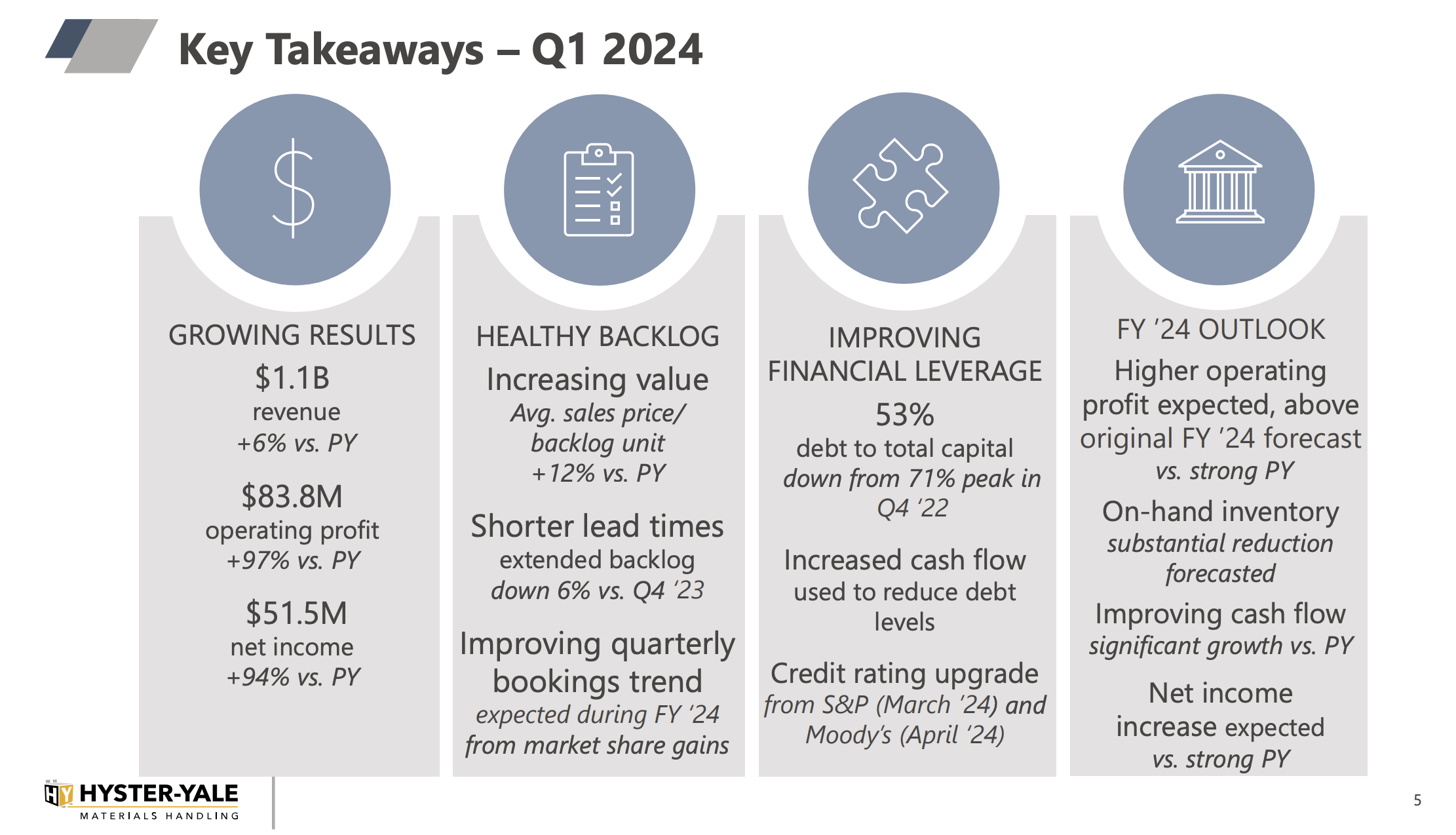

The firm released its first quarter 2024 earnings on May 7, and included these highlights, as displayed in the Q1 earnings presentation:

HY Q1 Key Takeaways (Q1 company presentation)

At the close on May 9, 2024, the share price was $79.01 and had a market cap of $1.28 billion.

Competition and competitive advantages

Hyster-Yale called itself “one of the leaders in the lift truck industry” when discussing market share domestically and internationally.

Other major lift truck and forklift companies include Toyota Motor Corporation (OTCPK:TOYOF), Kion Group AG (OTCPK:KIGRY), Jungheinrich Group (OTCPK:JGHAF), Clark Material Handling, and Komatsu Ltd. (OTCPK:KMTUY).

According to a report from Statista, Toyota held the largest market share in 2021 at 28.44%, and Kion was second with 13.78%. Hyster-Yale was the sixth largest with 5.67%.

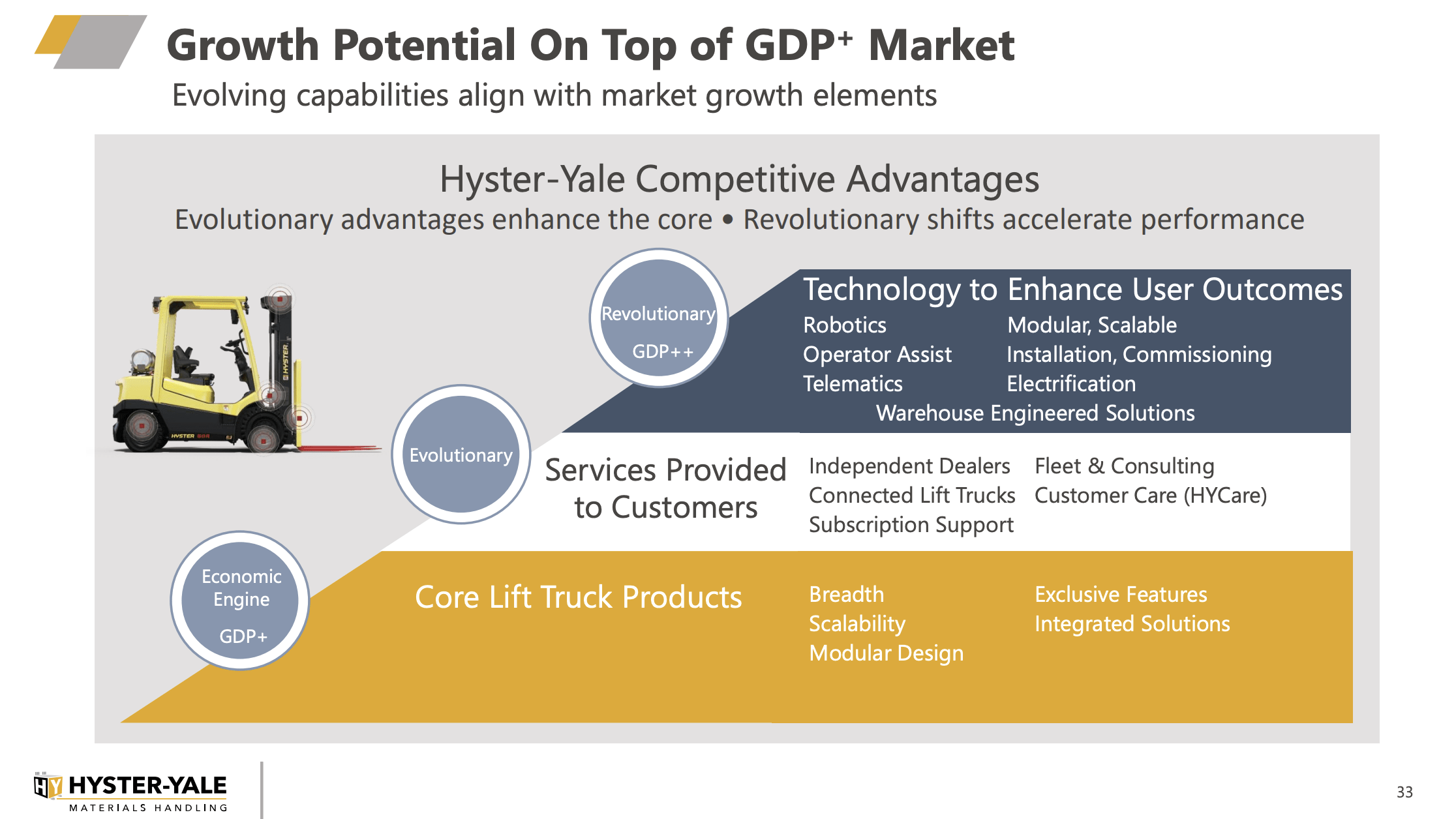

In the Q1 presentation, it argued that it has competitive advantages:

HY Competitive Advantages slide (Q1 investor presentation)

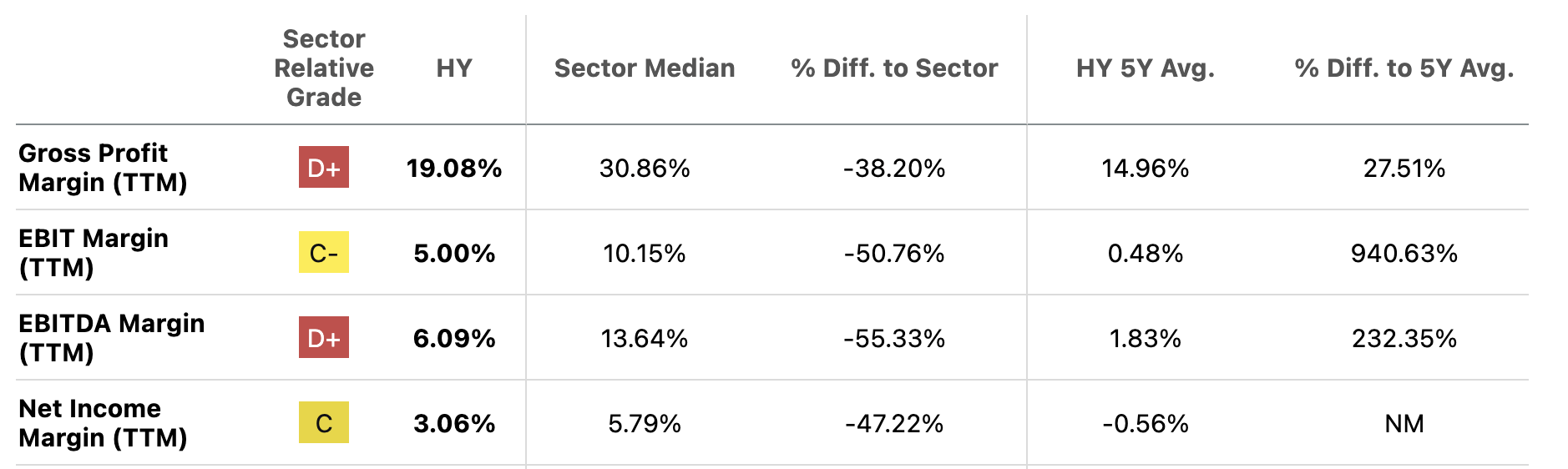

Hyster-Yale’s margins are generally below those of the Industrials sector medians, but they outperform on a five-year basis. It also does well when compared on returns (all TTM):

- Return on common equity: 42.37% versus 12.30% for the sector.

- Return on total capital: 14.16% compared to 7.20%.

- Return on total assets: 6.06% versus 4.85%.

Taken together, these metrics suggest a narrow to medium moat.

Margins

This excerpt from the Hyster-Yale profitability page at SeekingAlpha shows how the company is weak on a one-year basis, but strong on a five-year basis:

HY Profitability Margins (SeekingAlpha )

In the Q1-2024 earnings release, the company said the consolidated operating profit margin had grown to 7.9%, up from 4.3% in the same quarter last year. A big part of that gain came from a lift truck increase of 390 basis points, to 8.9%.

Hyster-Yale also pointed to “continued disciplined execution” and fewer low-margin legacy component sales at Bolzoni.

Going forward, the company noted in the earnings release that its goal is to be price competitive but maintain targeted booking margins. To do that, it plans to introduce new models and reduce its costs. Both Bolzoni and fuel cell subsidiary Nuvera are expected to deliver higher margins this year.

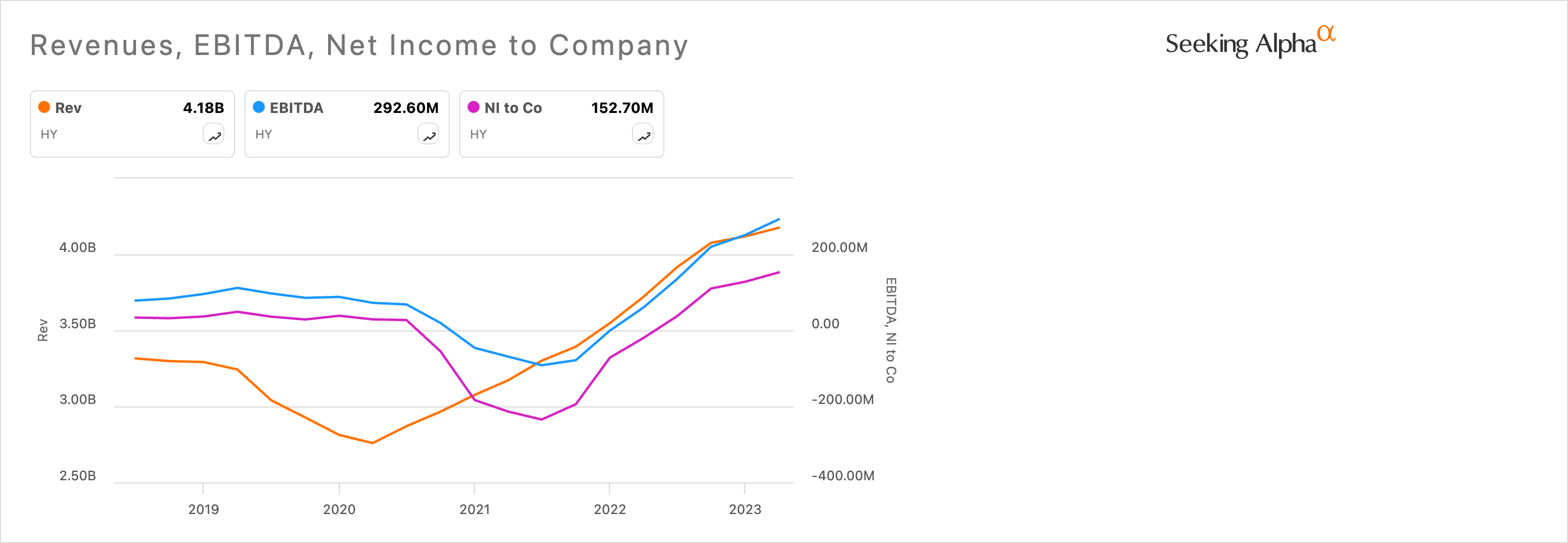

Growth

Like many other Industrials companies, Hyster-Yale’s revenue took a hit in 2020, while the EBITDA and net income effects were felt a year later. Management reported in the fourth-quarter 2021 earnings release, “Q4 2021 production continued to be severely disrupted by component and logistics availability.”

HY Revenue Ebitda Net Income chart (SeekingAlpha)

In its outlook statement for 2024, management noted in the Q1 earnings release that it expected improving quarter-over-quarter lift truck sales bookings throughout this year. It attributes the growth to expected gains in market share in the Americas and EMEA, and better North American market conditions in the second half.

For Bolzoni, the company expects revenue to be about the same as 2023’s, but to enjoy improved product margins. That will reflect higher-margin attachments and the phase out of legacy component sales to the lift truck segment.

Nuvera expects higher 2024 sales, with higher margins, but offset to some degree by higher development costs.

During the Q1 earnings call, President Rajiv Prasad said 2023 had been “an outstanding year” and Hyster-Yale was building on last year’s successes. He also noted that the firm had achieved an operating profit margin of more than 7% for the first time.

Hyster-Yale has not offered quantified estimates for 2024, but did say in its Q4-2023 earnings release that it expected its 2024 operating profit to increase, but net income would be about the same as in 2023, pulled down by higher income tax expenses.

A more optimistic outlook arrived with the Q1-2024 earnings release, with the firm saying that it now expected a higher operating profit, a substantial reduction in on-hand inventory, improving cash flow, and higher net income.

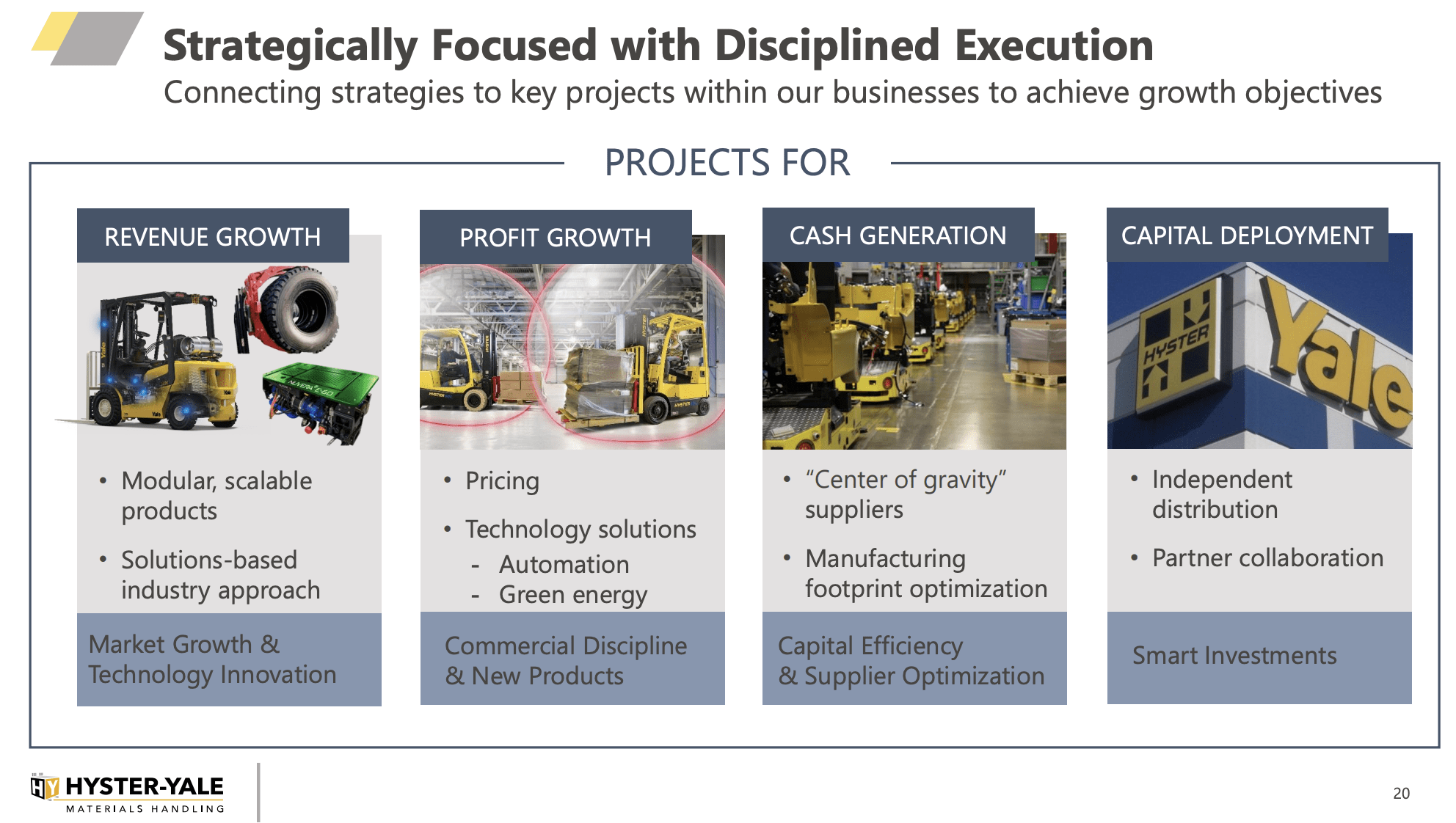

On a longer-term basis, the company has a set of strategies for growth:

HY Growth Strategies slide (Q1 investor presentation)

Hyster-Yale has a very slowly growing dividend. It went up in small increments from $0.31 in 2019 to $0.325 a year ago. Still, the current yield of 1.78% beats the S&P 500 average of 1.35%. The payout ratio is 15.06%, but don’t expect any significant increases in the near future as the company focuses on growth.

Management and strategy

Rajiv K. Prasad became the President and CEO in May 2023, after holding senior positions within the company. Previously he worked at Ford Motor Company (F), Lear Corporation (LEA), and International Truck and Engine Corporation.

Scott A. Minder is the Senior Vice President, CFO, and Treasurer at Hyster-Yale. Before joining the company in 2017 he held senior positions at PPG Industries, Inc. (PPG) and a division of Penske Automotive Group, Inc. (PAG).

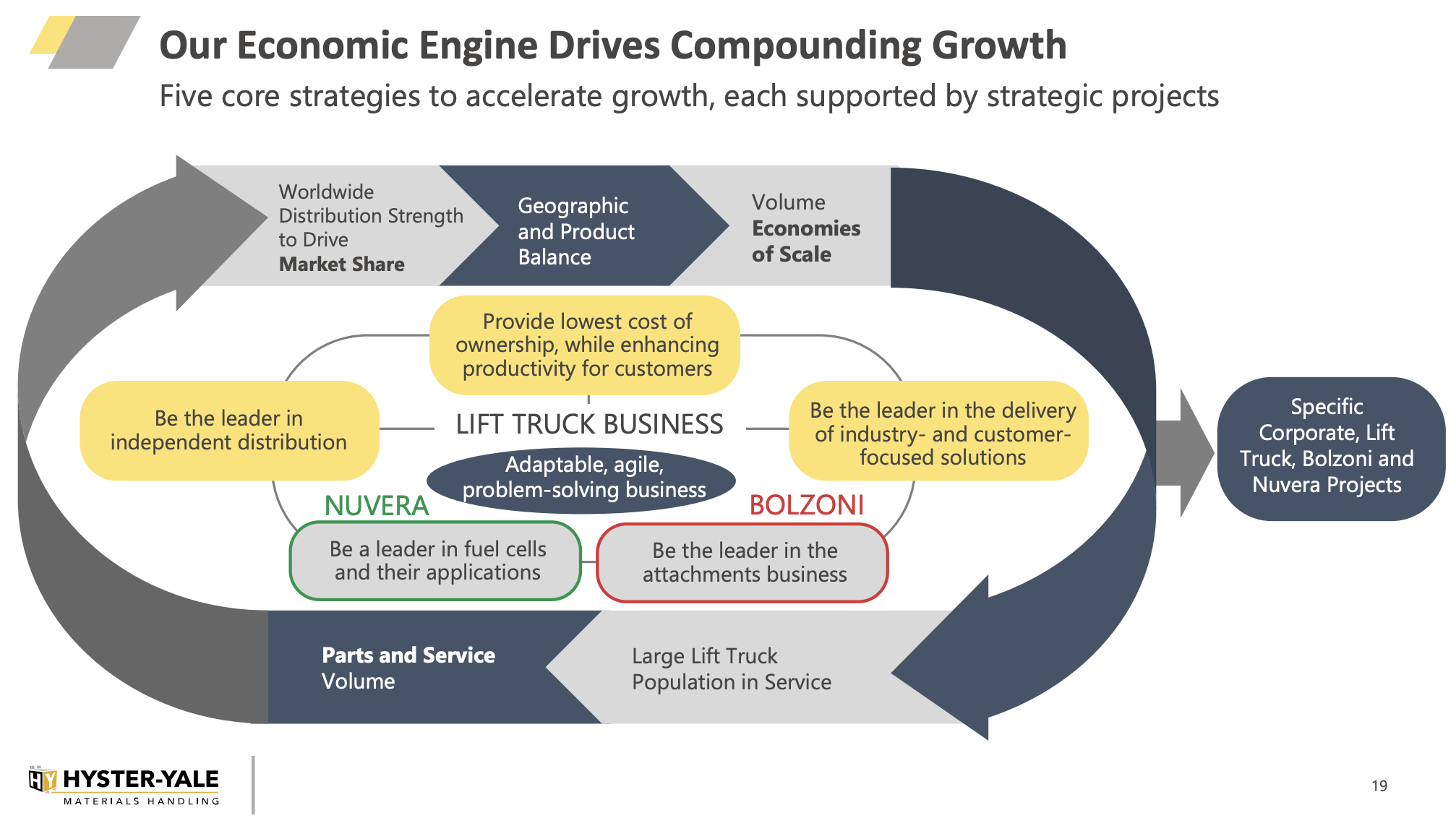

Within its objective of being a profitable growth company, it has a set of core strategies:

HY Growth Strategies slide (Q1 Investor Presentation)

The circular nature of the growth strategies suggests ongoing improvements, year after year. Across the top and down the right side we see strategies for expanding the lift truck business, while along the bottom of the inner circle, we see Bolzoni and Nuvera building on the strengths of the main lift truck business.

It’s a recipe that should work well for the company, as the individual components of the plan support each other.

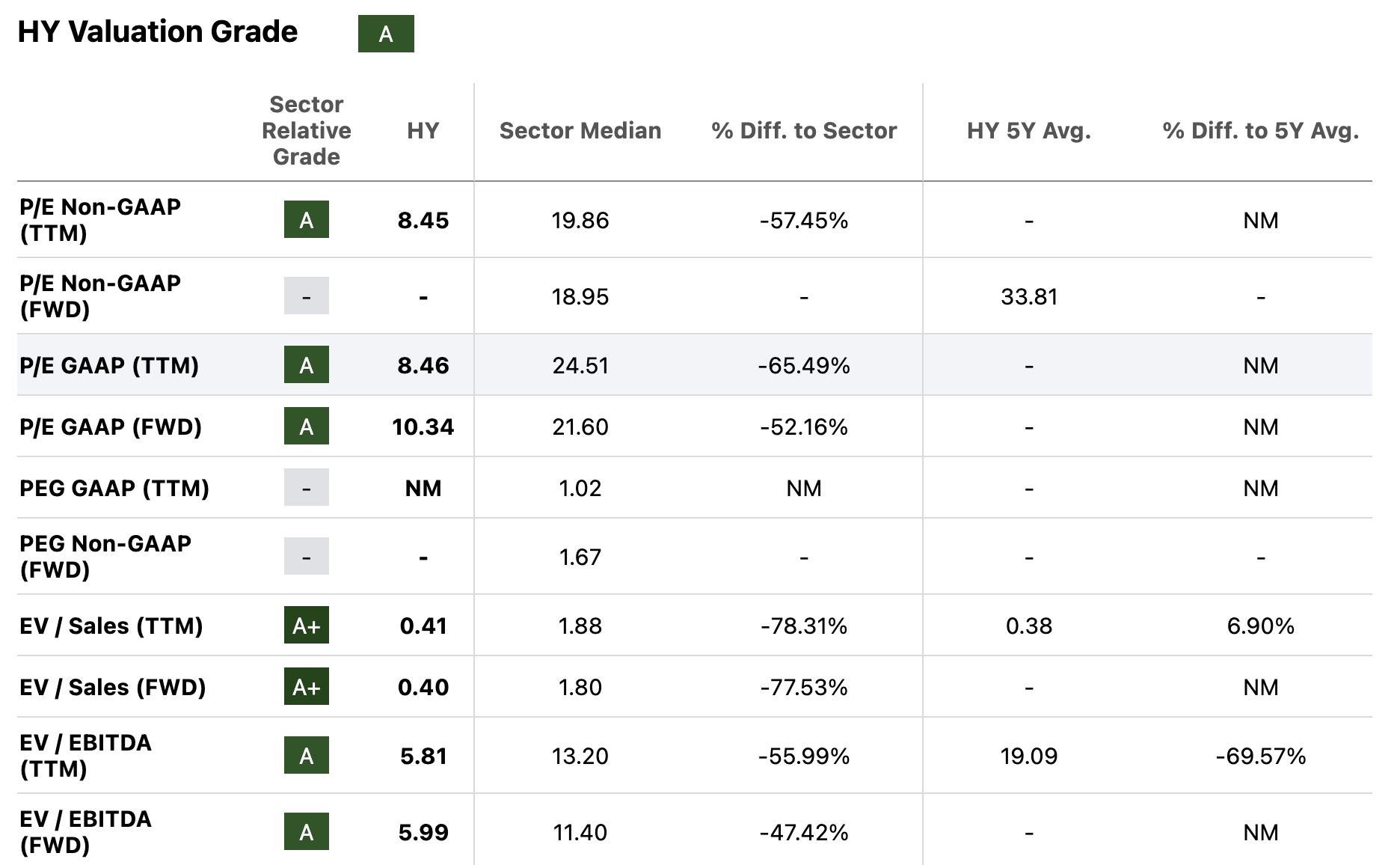

Valuation

This excerpt from the Hyster-Yale valuation page shows the firm is value-priced. All the key metrics are significantly lower than those of the Industrials medians:

HY Valuation table (SeekingAlpha )

Those undervaluation metrics come despite two days of big price jumps in response to the Q1 earnings report on May 7. The next day, the price increased by $13.90, or 23.55%, to close at $72.92. On May 9 it gained another $6.09, or 8.35%, to close at $79.01. Investors obviously see even more capital gains ahead.

From a technical perspective, it appears the share price has rebounded back to where it might have been if not for the plunge brought on by the Q4-2023 and full-year results reported on February 27:

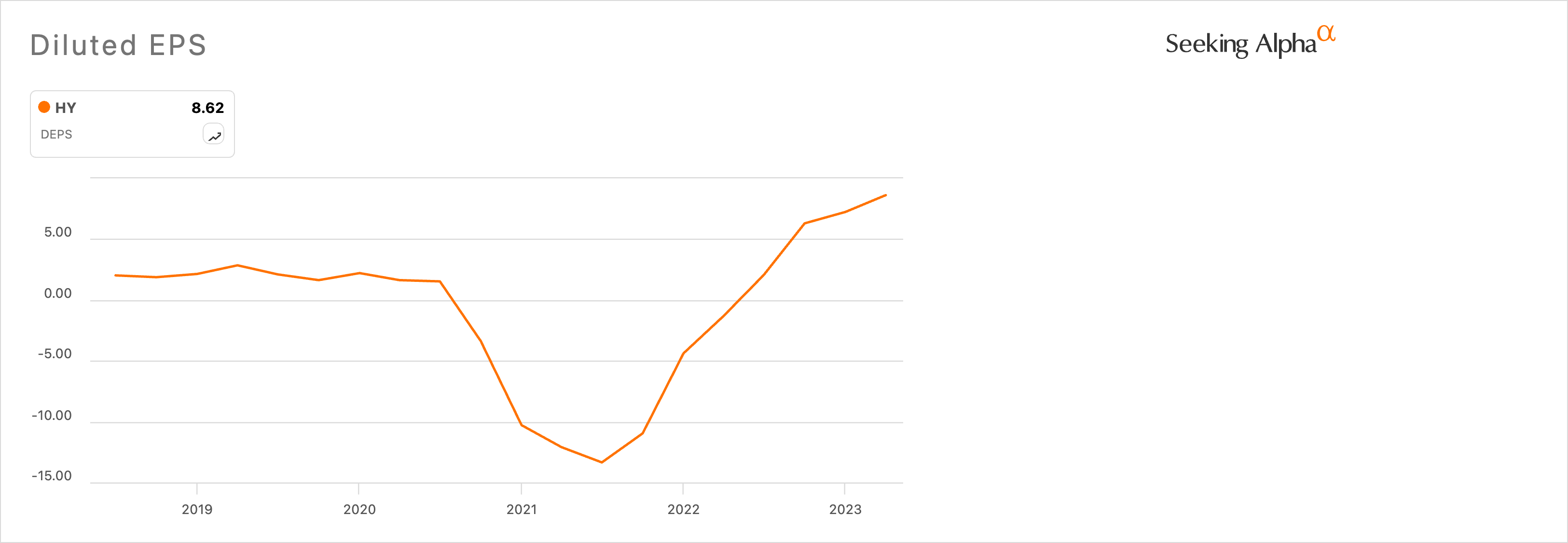

Over the past five years, diluted EPS growth has averaged 8.60% (according to Hyster-Yale’s growth page at SeekingAlpha). Most that growth has come in the past three years, as the company’s EPS recovered from the pandemic effects of supply chain and labor woes:

HY EPS chart (SeekingAlpha )

In its original guidance for 2024, Hyster-Yale indicated that it expected net income to remain about the same as it was last year, because of higher taxes. However, in the Q1-2024 release it upgraded that outlook; as noted in the earnings call, management expects higher quarter-over-quarter books throughout this year.

While the firm does not offer quantified guidance, I factor in their quarterly improvements, including better margins, and estimate EPS growth will be near the five-year average of 8.60%.

Assuming that price follows earnings, an 8.60% increase on the May 9 closing price of $79.01 would produce a one-year target price of $85.80.

Add the expected dividend yield of 1.78% to 8.60% for a total return of 10.38%. That leads to me to give Hyster-Yale a Buy rating. The Quant system has a Hold rating, while Wall Street analysts have one Buy and one Strong Buy. No other SeekingAlpha analysts have rated the firm in the past 90 days.

Risk factors

Individual shareholders may have little influence at the boardroom table. According to the 10-K, some members of the extended founding family control 72% of the Class A and Class B shares. Class A shares, available to the public, have one vote each, while holders of Class B shares get ten votes for each share, giving the latter control.

The lift truck business historically has been cyclical, and therefore, orders rise and fall according to the state of the world economy. Customers delay new lift truck and parts purchases during economic downturns. As we saw, Hyster-Yale’s net income dropped dramatically as a result of pandemic-driven economies a few years ago.

The company now operates worldwide, meaning it deals in multiple currencies, and as a result is exposed to potentially higher costs and lower returns because of currency exchange rates. Similarly, normally smooth international operations may be disrupted by anything from new tariffs to the outbreak of wars.

There are a limited number of suppliers for some critical components, including diesel, gas, and fuel cell engines, as well as the counterweights used to counterbalance some lift trucks. While most components are readily available, it has experienced shortage of key components in the past.

The competition for lift trucks and aftermarket parts is described as “intense”, and some of the other players may have lower manufacturing costs, and/or greater financial resources. They also operate in worldwide markets, like Hyster-Yale.

Conclusion

Investors returned Hyster-Yale, in droves, after the Q1-2024 earnings were released on May 7. In doing so, the stock price reverted to the mean or in some way got the share price back on its previous track.

This is a strong company, and the odds are high that it will continue to generate ongoing capital gains for both long-term and recent investors. It is executing on plans to grow its core and ancillary businesses, as well as improve its margins.

Hyster-Yale is a Buy.

{kind=link}